2023 Federal Budget Highlights

On March 28, 2023, Deputy Prime Minister and Minister of Finance, Chrystia Freeland, presented the federal budget for the 2023-2024 fiscal year. We have summarized selected highlights of the personal and business tax measures.

Contact us if you have any questions regarding the information in this article.

INDIVIDUALS

Expansion of the Alternative Minimum Tax Base

Increase to Registered Education Savings Plan Withdrawal Limits

Extension of Registered Disability Savings Plan Representative Rules

Introduction of the Grocery Rebate

Taxpayer Information Sharing for the Canadian Dental Care Plan

Deduction for Tradespeople’s Tool Expenses

BUSINESS

Strengthening the Intergenerational Business Transfer Framework

Changes to Employee Ownership Trust Rules

Introduction of Tax on Share Buybacks

INDIVIDUALS

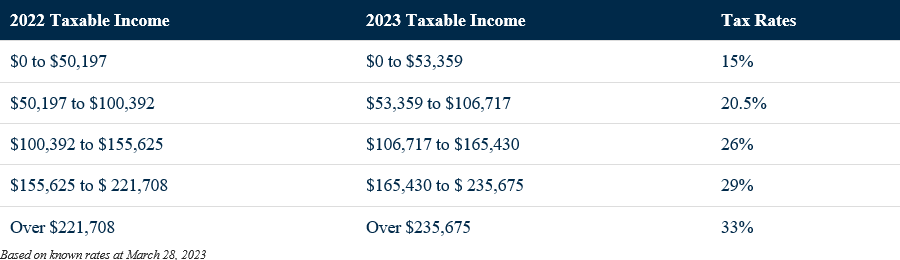

Personal Tax Rates

The budget did not propose any changes to individual income tax rates other than the alternative minimum tax rates discussed later.

Expansion of the Alternative Minimum Tax Base

- The budget proposes to change the calculation of alternative minimum tax (AMT) to better target high-income individuals starting in tax years that begin after 2023.

- It proposes to increase the AMT exemption from $40,000 to the start of the fourth federal tax bracket, indexed annually to inflation. The estimated 2024 exemption would be approximately $173,000.

- The AMT rate would increase from 15 per cent to 20.5 per cent to correspond with the second federal income tax bracket.

- The following are proposed changes to income inclusion rates:

- 100 per cent inclusion rate for capital gains, up from 80 per cent

- 50 per cent application rate for capital loss carry forwards and allowable business investment losses

- 100 per cent inclusion rate for stock option employment benefits

- 30 per cent inclusion rate for capital gains on donations of publicly listed securities

- 30 per cent inclusion rate for employment stock option benefits from the donation of the underlying publicly listed securities

- The lifetime capital gains exemption will remain at a 30 per cent inclusion rate.

- Proposed changes to deduction rates would disallow 50 per cent of the following deductions:

- employment expenses, other than those who earn commission income

- deductions for Canada Pension Plan, Quebec Pension Plan, and Provincial Parental Insurance Plan contributions

- moving expenses

- child care expenses

- disability supports deduction

- deduction for workers’ compensation payments

- deduction for social assistance payments

- deduction for Guaranteed Income Supplement and Allowance payments

- Canadian armed forces personnel and police deduction

- interest and carrying charges incurred to earn income from property

- deduction for limited partnership losses of other years

- non-capital loss carryovers

- Northern residents deductions

- Most credits would apply at 50 per cent against AMT instead of 100 per cent.

- An exception is the Special Foreign Tax Credit that will continue to be 100 per cent.

- The proposed AMT will continue to use the actual dividend amount (not gross-up) and fully disallow the dividend tax credit.

- The seven-year carry forward period for the recovery of AMT will not change.

- AMT will continue to be not applicable to an individual in the year of death.

- Trusts that are currently exempt from AMT will continue to be exempt and the government will continue to examine whether additional types of trusts should be exempt from AMT.

Increase to Registered Education Savings Plan Withdrawal Limits

- The budget increases the educational assistance payment (EAP) limit for the first 13 consecutive weeks of full-time enrollment from $5,000 to $8,000 and from $2,500 to $4,000 for part-time enrollment.

- The changes would come into force on March 28, 2023.

- Individuals who withdrew previous EAPs in 2023 may be able to withdraw an additional EAP amount.

- The budget also proposes to allow divorced or separated parents to open joint RESPs, effective March 28, 2023.

Extension of Registered Disability Savings Plan Representative Rules

- The budget expands the qualifying family member exception by three years to December 31, 2026.

- The federal government hopes the provinces and territories will examine how they can better accommodate the needs of RDSP beneficiaries by developing solutions to address RDSP legal representative issues.

- The budget also proposes to broaden the definition of a ‘qualifying family member’ to include a sibling of the beneficiary who is age 18 or older.

Introduction of the Grocery Rebate

- The Grocery Rebate targets modest-income individuals who currently collect GST credit (GSTC) payments.

- Those individuals will receive an additional GSTC amount equal to twice the amount received for January 2023.

- The maximum amounts under the Grocery Rebate are:

- $153 per adult

- $81 per child

- $81 for the single supplement

- The government will pay the amounts as soon as possible following passage of legislation.

Taxpayer Information Sharing for the Canadian Dental Care Plan

- The budget proposes to provide legislative authority to the Canada Revenue Agency to share taxpayer information with officials of Health Canada and Employment and Social Development Canada to administer and enforce the new Canadian Dental Care Plan.

Deduction for Tradespeople’s Tool Expenses

- The budget proposes to double the maximum employment deduction for tradespeople’s tools from $500 to $1,000, effective for 2023 and subsequent taxation years.

- The change means that extraordinary tool costs that are eligible for deduction under the apprentice vehicle mechanics’ tools deduction would be costs that exceed the combined amount of the tradespeople’s tools ($1,000) and the Canada Employment Credit ($1,368 in 2023) or five per cent of the taxpayer’s income earned as an apprentice mechanic, whichever is greater.

BUSINESSES

The budget did not propose any changes to federal corporate income tax rates or to the $500,000 small business limit.

Federal Corporate Tax Rates

Strengthening the Intergenerational Business Transfer Framework

- The budget proposes to tighten the rules around intergenerational share transfers so that capital gains treatment only applies to genuine business transfers to a child or grandchild’s purchaser corporation.

- The government proposes the following additional conditions where taxpayers can choose one of two transfer options:

- an immediate intergenerational business transfer (three-year test) based on arm’s length sale terms; or

- a gradual intergenerational business transfer (five-to-ten-year test) based on traditional estate freeze characteristics

- Refer to the budget document for the test condition details.

- The limitation period for reassessing a transferor’s tax liability would be extended by three years for an immediate business transfer and by 10 years for a gradual business transfer.

Changes to Employee Ownership Trust Rules

- The budget proposes new rules to facilitate the use of employee ownership trusts (EOT) to acquire and hold shares of a business as part of a succession plan.

- The five-year capital gains reserve would be extended to a 10-year reserve for qualifying business transfers to an EOT.

- There would be an extension to the repayment period of a shareholder loan from one year to 15 years for amounts loaned to the EOT from a qualifying business to purchase shares in a qualifying business transfer.

- EOTs would be exempt from the 21-year deemed disposition rule while it meets the conditions to be an EOT.

- These measures would apply as of January 1, 2024.

Introduction of Tax on Share Buybacks

- A two per cent tax applies to the net value of all types of share repurchases by public corporations in Canada listed on a designated stock exchange, effective January 1, 2024.

- Mutual funds are not subject to the repurchase tax.

- The tax would apply to real estate investments trusts, specified flow-through trusts, and SIFT partnerships if they have units listed on a designated stock exchange.

- The tax does not apply to an entity if it repurchased less than $1 million of equity during that taxation year.

Green Economy Initiatives

The budget introduces and expands a number of tax credit programs for green initiatives:

- New investment tax credit for clean hydrogen

- Clean technology investment tax credit expanded to geothermal energy

- Expansion of labour requirement to the clean electricity investment tax credit and the investment tax credit for carbon capture, utilization, and storage

- New investment tax credit for clean technology manufacturing

- Expansion of the zero-emission technology manufacturers tax reduction to include nuclear manufacturing for nuclear energy equipment, processing or recycling of nuclear fuels and heavy water, and manufacturing of nuclear fuel rods

- Extension of the zero-emission technology manufacturers tax reduction to 2034

- Dual use equipment that produces heat and/or power or uses water that is used for carbon capture, utilization, and storage (CCUS) would be eligible for the CCUS tax credit

- Expansion of the eligibility for the critical mineral exploration tax credit (CMETC) to lithium from brines would apply to flow-through share agreements entered into after March 28, 2023 and before April 2027

Refer to the official Budget 2023 document for further details on the above tax announcements.

Please click on the button below to subscribe to our mailing list.

By subscribing, you will get regular commentary about our portfolio holdings, market outlook, financial planning, and events. You can withdraw from receiving emails at any time by unsubscribing.

Please contact us if you have any questions relating to the information in this article.

Information in this article is from sources believed to be reliable, however, we cannot represent that it is accurate or complete. It is provided as a general source of information and should not be considered personal investment advice or solicitation to buy or sell securities. Raymond James advisors are not tax advisors and we recommend that clients seek independent advice from a professional advisor on tax-related matters. The views are those of the author, Marnoa Private Wealth, and not necessarily those of Raymond James Ltd. Investors considering any investment should consult with their Investment Advisor to ensure that it is suitable for the investor’s circumstances and risk tolerance before making any investment decision. Raymond James Ltd. is a Member - Canadian Investor Protection Fund.