The $600 Billion AI Spending Bet: Hyperscalers Are Powering a Trillion‑Dollar Reinvention of Productivity

- By Christopher De Sousa, CIM® | Portfolio Manager

- 6 Min Read

Share This Post

Market volatility rose in the fourth quarter of 2025, driven mainly by global trade tensions and concerns over a potential AI bubble. Volatility has continued into the new year but the U.S. economy remains well positioned. Key tailwinds include ongoing fiscal stimulus through the One Big Beautiful Bill Act (OBBBA), cumulative monetary easing with several rate cuts over the past 18 months, and continued deregulation supporting corporate profitability. Favorable wealth effects and productivity gains linked to AI adoption have also buoyed sentiment. However, geopolitically induced market volatility will likely remain a prominent theme in 2026.

Spotlight on Artificial Intelligence

Elsewhere, the market remains focused on assessing the scale and sustainability of AI-related infrastructure spending, with future capital returns continuing to be a central topic of discussion. Against this backdrop, the five major AI hyperscalers—Alphabet, Meta, Microsoft, Oracle, and Amazon—show no signs of scaling back their capital expenditure programs. These investments have fueled robust revenue and earnings growth, though results remain constrained by shortages in chips, data center, and electricity capacity.

From our perspective, rising demand and expanding backlogs for high-performance cloud computing and AI workloads continue to support the current investment cycle and the push to deploy additional capacity. The U.S. hyperscalers plan to maintain elevated capital expenditures through 2026 and beyond as they expand data center and power infrastructure as well as secure next-generation AI hardware and chips. The U.S. hyperscalers expect to spend more than $600 billion in 2026. But the actual figure may prove much higher as analysts have consistently underestimated AI-related capital spending.

Big Tech Balance Sheet Risks?

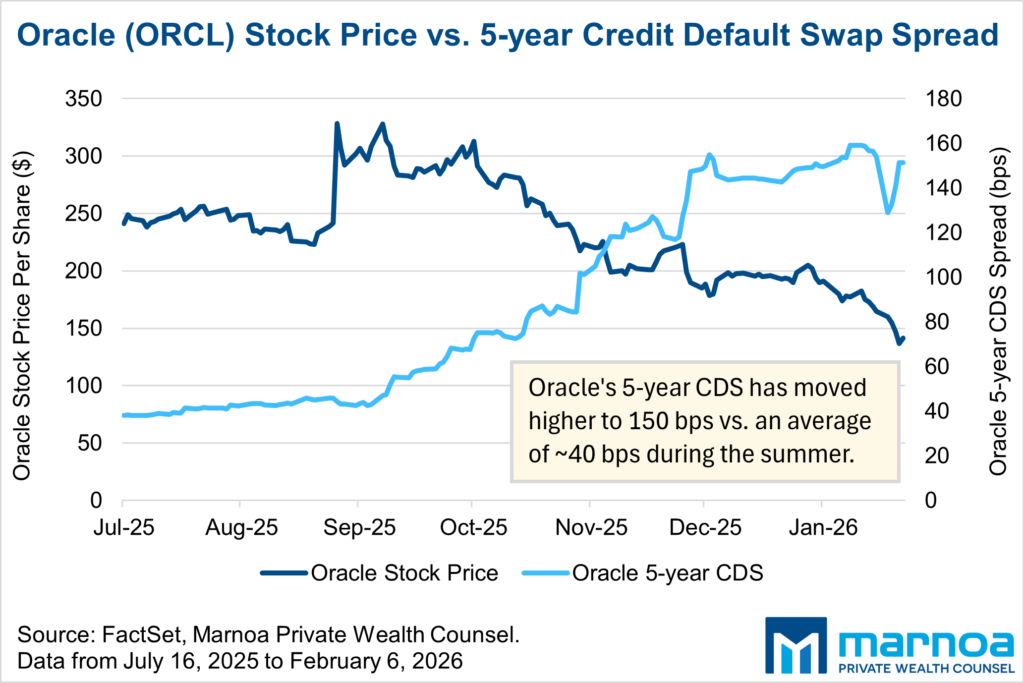

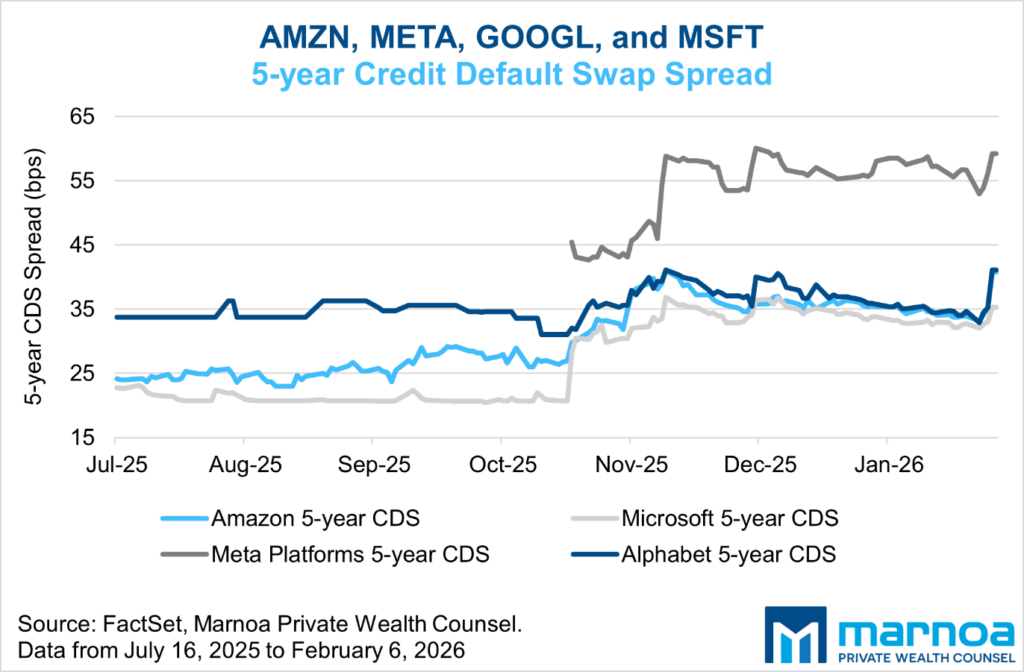

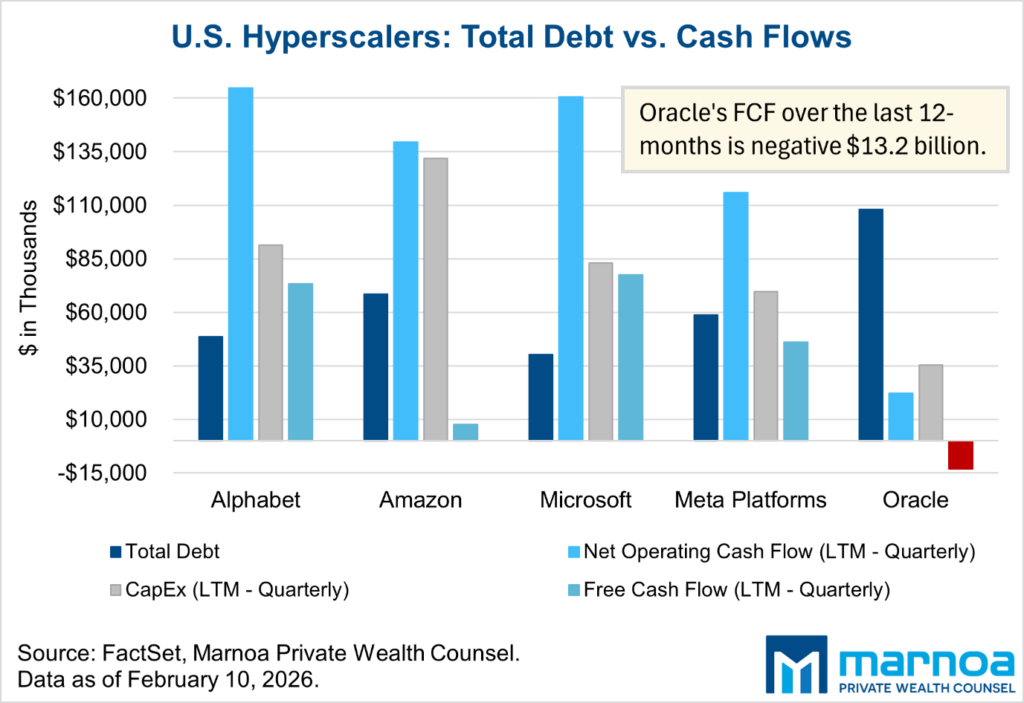

The U.S. hyperscalers have strong balance sheets and substantial internal cash generation, which enable them to sustain high and increasing levels of capital expenditure on AI and cloud infrastructure. Oracle, however, stands as an outlier. Its AI-related spending has coincided with significantly greater reliance on debt financing. Oracle fails to generate adequate internal cash flow to sustain these projects, as capital expenditures have outpaced operating cash inflows. As a result, Oracle’s free cash flow has turned negative, and the cost of insuring Oracle’s debt against default has surged (see chart below).

Oracle’s mounting debt pile, which now stand at just over $100 billion, have pushed up the cost of the company’s credit default swaps (CDS) over the past six months, reaching their highest levels since 2009 and far exceeding those of its peers (see chart below). A CDS quoting at 150 basis points (bps) means paying 1.50% per year of the bond’s insured value. For example, the cost of insuring $10 million in Oracle bonds against default has climbed to about $150,000 annually—up from roughly $40,000 during the summer months. Bond investors normally expect regular interest payments and the return of their principal at maturity. But neither is guaranteed. They shoulder the risk of the company’s creditworthiness. To hedge that risk, some investors turn to CDS, a financial instrument that functions much like insurance against default.

While strong operating cash flows from the U.S. hyperscalers (excluding Oracle) remain the primary funding source for AI investments, debt markets are playing an increasingly supportive role (see chart below). In 2025, the five major hyperscalers issued $121 billion in U.S. corporate bonds—up sharply from the $28 billion annual average between 2020 and 2024, according to BofA Securities. All in all, this marks a clear shift from the hyperscalers’ historically asset‑light model (i.e., lower capital expenditure intensity) toward one defined by higher capital intensity and large on‑balance‑sheet AI infrastructure. The result is a structural rise in depreciation costs, modest pressure on operating margins, and greater leverage risk.

Interest rate cuts should reduce borrowing costs and encourage debt financing to supplement cash flows from operations. BofA Securities expects the hyperscalers will borrow about $140 billion annually over the next three years to fund AI investments, potentially exceeding $300 billion annually. An accommodative low-rate environment should sustain momentum for data center buildouts, power grid expansions, and related infrastructure projects in global regions. To quantify the scale of investment, Nvidia CEO Jensen Huang estimated that global AI infrastructure spending could reach $3 trillion to $4 trillion by 2030.

How Big Is the Opportunity?

One might ask why the hyperscalers and other technology companies are increasing leverage and committing billions of dollars to a new technology. Is the opportunity truly that large?

According to the International Monetary Fund, global GDP stands at roughly $117 trillion and is expected to grow to about $150 trillion by the end of the decade. Meanwhile, Gartner projects worldwide IT spending to total $6.08 trillion in 2026, an increase of 9.8% from $5.54 trillion in 2025—accounting for just over 5% of global GDP. We expect global IT spending to rise as a share of global GDP as technology continues to replace human labour and drive greater demand for IT infrastructure, software, and digital services. This trend is reinforced by a study from the McKinsey Global Institute, which found that 50% of human labour activities globally could potentially be automated using technology.

AI is rapidly becoming a central enabler of productivity‑driven digital transformation. It is reshaping entire industries, unlocking new markets, and contributing to global economic output at a great scale. With rapid advances in both agentic (autonomous task execution without human oversight) and physical AI (robotics and humanoids), technology is poised to capture a larger share of human labour output and represent an expanding portion of global GDP over time.

A McKinsey Global Institute study focused on the U.S. economy, titled “Agents, Robots, and Us: Skill Partnerships in the Age of AI,” finds that current technologies can theoretically automate about 57% of U.S. work hours today. The study highlights that AI-powered agents could perform around 44% of non-physical tasks, while robots could automate roughly 13% of physical work. Overall, about 40% of U.S. jobs fall into occupations with the highest potential for automation by agents or robots.

So, circling back to the question: is the opportunity truly that large? Yes, it’s measured in the trillions.

Even though AI systems such as large language models and generative tools have advanced rapidly since the debut of ChatGPT in late 2022, we’re still exploring how to apply them effectively. As with every major technological shift before it, some early use cases will deliver clear, measurable returns and value, while many others will eventually fall short and fail.

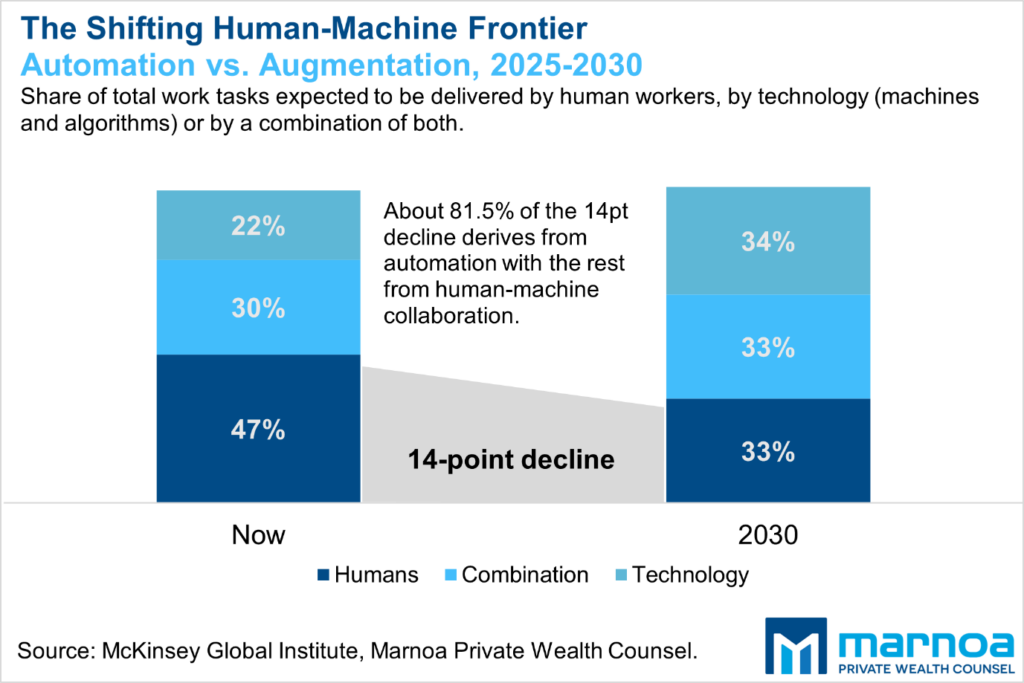

The World Economic Forum’s Future of Jobs Report 2025 highlights that humans currently perform 47% of all work tasks globally, while technology such as machines and algorithms handle 22%. The remaining share involves a mix of human and technological input. By 2030, employers anticipate that work will be evenly distributed among these three categories (see chart below). The report further indicates that nearly 82% of the projected 14‑point decline in human task share between 2025 and 2030 will result from increased automation.

Final Remarks

The transition from human labour to machine-driven productivity represents a multi‑trillion‑dollar economic opportunity. That is why U.S. hyperscalers and other leading technology companies around the world are racing to invest in both agentic and physical AI technologies. In our view, the opportunity to capture even a small fraction of global GDP through automation and digital transformation underpins why hyperscalers are investing heavily in AI. This secular trend is why we own positions in the market leaders—Amazon, Alphabet (Google), Nvidia, Microsoft, and Meta—that enable these technologies today and shape their future impact.†

Christopher De Sousa, CIM®

Portfolio Manager

(519) 707-0053

www.marnoa.ca

† This commentary is provided for informational purposes only and reflects the author’s views as of the date of publication. Statements regarding market conditions, company fundamentals, or future outcomes are forward-looking and subject to change without notice. There is no guarantee that any investment strategy or expectation discussed will be successful. References to specific securities are for illustrative purposes only and do not constitute a recommendation to buy or sell any security.

March 31, 2026

Every Storm Runs Out of Rain